No, they are not working. Yes, they could be effective. But the 886-page climate risk and greenhouse gas (GHG) emissions disclosure “final rule” that was approved last week by the US Securities and Exchange Commission (SEC) does not help. In the SEC’s March 6 press release, Chair Gensler said, “These…rules will provide investors with consistent, comparable, and decision-useful information, and issuers with clear reporting requirements.” But, at least so far, they don’t.

“ESG”—Environmental, Social and Governance—is a term that emerged in the early 2000s, as an offshoot of the Corporate Sustainability and “EHS” (Environment, Health and Safety) movements of the 1990s. The idea is to convert these concepts into measurable, reportable metrics, or “ESG scores”, and has become a favorite topic from Davos to Aspen over the last 15 years. Initially, the focus was on the “Green Bond” market. What makes a bond truly green, anyway, as opposed to just another form of green-washing? The Big Six consultancies have since invested significant time and resources into the development of complex, 100+ page ESG reporting frameworks. The result is a plethora of inconsistent metrics communicated in long, hard-to-digest reports which do not enable any apples-to-apples inter-company GHG performance comparisons.

In what appears to have started as an attempt to make ESG performance measurement simpler for the reporting companies and more transparent and understandable for the retail investor--at least when it comes to greenhouse gas emissions (GHGs) and climate risk disclosures--the SEC is now proposing to perpetuate an expensive, confusing system that delivers unprecedented market power to the advisors and consultants, mostly at the expense of the retail investors.

Let’s skip to the punchline. In 2022, 100% of global energy production and end use-related GHGs totalled just under 37 billion TCO2e. If we count energy producers’ direct operating emissions, plus the GHGs that are released into the atmosphere when the energy products are ultimately used, in 2022 less than 150 companies and the final users of their products, were responsible for roughly 30 billion TCO2—or over 80% of total energy-related GHGs.

Why are we talking about disclosure rules with which 10s of 1,000s of companies must comply, when what informed investors need to see, regularly, is a comparison of the GHG price that all of society is paying for the earnings that are generated by less than 150 companies when they sell their products?

To make informed decisions, investors need to see companies’ operations broken into five general sectors, so that it is easy to see which companies are delivering the best value, relative to their competitors, for every TCO2e of heat-trapping gas they are causing to be added to our atmosphere. I think all of the public companies that are Major Emitters should break their operations into 6 target market classes: (1) energy, (2) building products (including fabricated metals, glass and plastics), (3) chemicals (including fertilizers), (4) minerals, (5) compute power and (6) food.

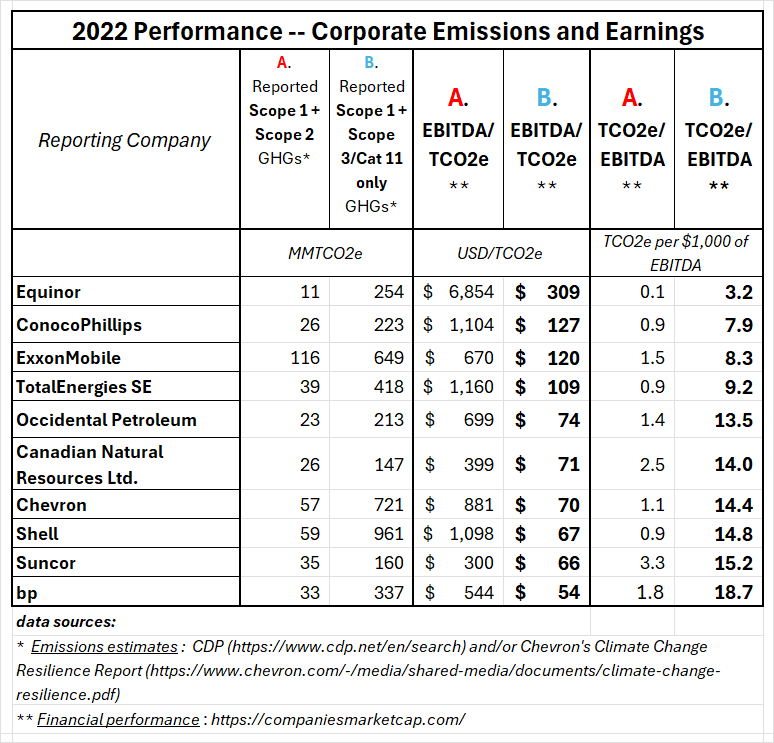

Then, it should be fairly easy to see how different corporate subdivisions compare, in GHG performance terms, to others in the same class, and how they are trending, over time. See a snapshot, below, of the kind of information all investors should be able to access with ease.

In the world of ESG consultants, GHGs released directly from the companies’ direct operations are called “Scope 1” emissions. “Scope 2” includes emissions released in the production and transport of the energy the companies use in their operating facilities. Any one company’s Scope 2 emissions are another company’s Scope 1 emissions.

“Scope 3” emissions include all other emissions that happen anywhere in the reporting company’s supply chain and in the processing, transport and distribution of their products/services to their ultimate customers. Scope 3 emissions are broken into 15 “categories.” Category 11 is called “use of sold products” and accounts only for the emissions that are released when the supplied product is used.

It is very difficult and costly for a company to develop reliable estimates for all of the emissions included in the definition of Scope 3. But, most of the time, Category 11 emissions are pretty easy for most of the Major Emitters to estimate and report and are the most material component of Scope 3.

Personally, I don’t care about Scope 2. I want to see regular updates of Major Emitters’ Scope 1 and Scope 3 Category 11 (only) GHGs. I want to see which corporate operating divisions, in each of the 6 classes, are earning the highest returns per TCO2e of GHGs released to the atmosphere. I also want to see how many GHGs it is costing to deliver each $1,000 of earnings that translate into investor returns.

Why should I invest in an energy company that is discharging 18.7 TCO2e per $1,000s of earnings when I can invest in and also buy my energy from a competitor that is discharging less than half that amount? (Note, in passing, that the 10 companies in the table, above, and their customers, accounted for over 11% of global energy sector GHGs in 2022.)

So, all the SEC needs to order, in their final rule, is:

- Every public company for whom Scope 1 GHGs for their global ops total more than 1,000,000 TCO2e/year shall include their Scope 1 + product sales (Scope 3/Category 11) GHGs, as well as TCO2e/$1,000 of EBITDA, at the bottom of the Operating Statement in their quarterly and annual financial reports.

Ideally, they will also include a table that breaks down reported GHGs and TCO22/$1,000 or EBITDA, by country where the product is ultimately consumed, in their notes to the Operating Statement. But that geographic breakdown does not have to be mandated by the SEC.

- Every public company that has ever reported to the CDP must report their Scope 1 + product sales GHGs to the SEC, even if they do not meet the 1,000,000 TCO2e/year GHG threshold outlined in item #1.

- Any company that includes proved and/or unproved Fossil Fuel reserve values on the asset side of their Balance Sheet shall also include an estimate of the product end use GHGs that would be realized if all of those FF reserves were converted into finished products, assuming (for consistency in reporting purposes) no change from the current finished product mix for the company's future sales.

If the reporting company wishes to forecast different product mixes in future sales, and show the potential impacts on the asset valuations as well as projected TCO2e/$1,000 of EBITDA impacts, they are free to include such analyses in the notes to their Operating Statement and Balance Sheet. But the reporting standard should reflect the "no change in sales portfolio product mix" assumption.

All estimates should show both gross (actual emissions) and net (after accounting for credit purchases to offset actual emissions).

In other words, it shouldn’t take 886 words to write the very much needed new SEC rule, let alone 886 pages.